The year started for China with a positive tone on the back of a turnaround in private sector sentiment, driven by a more supportive economic policy mix, optimism around the country’s capabilities on artificial intelligence (AI), and a stabilization in manufacturing activity. Importantly, this came after years of subdued investor appetite and volatile growth on the back of real estate wounds, regulatory stringency, limited official stimulus, and the trauma from hard pandemic lockdowns.

Such positive outlook and turnaround translated into stronger activity and constant upgrades in growth expectations since September 2024. However, global macro prospects were suddenly shaken by a radical shift in US trade policies in February, when president Trump announced a massive increase in import tariffs. China, in particular, was singled out by the US with “embargo like” 140% tariffs and much less room for exemptions. After bilateral negotiations started, tariffs were reduced to a more manageable but still high 40% rate.

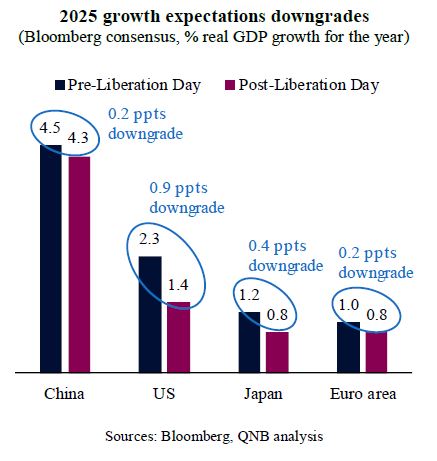

Despite this major shock, China’s economy appears to be resilient. In fact, across major economies, China seems to be the least affected by growth expectations downgrades since US tariffs “Liberation Day,” even if the country is by far the largest exporter globally.

In our view, three main factors sustain a more optimistic economic take on China in the face of the US policy shock.

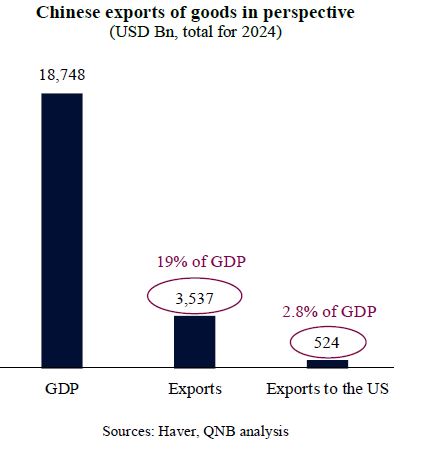

First, despite being the world’s largest exporter and a key node in global manufacturing, the overall impact from US tariffs on China’s growth is very limited. This is largely due to the declining importance of the US as an export destination and Beijing’s strategic reorientation of trade flows. In the early 2000s, the US accounted for nearly 20% of Chinese exports, but this share has declined to around 15% in recent years, equivalent to around 2.8% of the country’s GDP. Exports grew stronger in markets such as Southeast Asia, the EU, and Belt and Road countries, helping to offset US-driven losses. Moreover, exports themselves have been declining in overall importance to China’s economic model, now contributing less than 20% to GDP – compared to 35% in 2006 – amid a policy-led pivot toward domestic consumption, high-tech innovation, and services. These structural shifts, coupled with adaptive trade strategies, have helped insulate China from the full brunt of Trump-era tariffs, reducing their macroeconomic impact and sustaining the country’s external surplus.

Second, tariffs are blunt tools in a world of fragmented supply chains, and China’s central role in global production networks has significantly diluted their effectiveness. Unlike the bilateral trade flows of the past, modern goods cross multiple borders during assembly, making it hard to isolate national value added. Multinational firms adapt quickly, shifting final assembly to third countries while maintaining Chinese inputs through transhipment. These workarounds often outpace enforcement, undermining the intent of protectionist policies. Additionally, a substantial share of Chinese exports – such as critical components in electronics, machinery, and pharmaceuticals – are not easily substitutable and remain essential to US firms and supply stability. As a result, tariffs are unlikely to trigger reshoring and China is expected to retain its role as an indispensable link in global manufacturing.

Third, US tariffs are expected to be offset by the devaluation of the Chinese renminbi (RMB), particularly in real effective terms, which is enhancing China’s price competitiveness globally. Since the escalation of the “trade war” in February, the RMB has weakened against the USD, but even more so against a broader basket of currencies, resulting in a meaningful depreciation of China’s real effective exchange rate (REER). This has lowered the relative cost of Chinese exports in non-USD markets, helping Chinese firms gain market share globally despite higher US tariffs. The REER adjustment acts as an automatic stabilizer for China. In effect, the RMB’s adjustment is helping to preserve or even increase external demand, ensuring continued export surplus, further underscoring the limitations of unilateral trade barriers.

All in all, China’s growth prospects this year remain moderately robust despite continued trade tensions. This is due to a structural decline in US export dependence, the ineffectiveness of tariffs in a globalized supply chain environment, and the competitive tailwind from a weaker RMB collectively cushioning the Chinese economy from material external shocks.

Download the PDF version of this weekly commentary in

English

or

عربي