The One Big Beautiful Bill (OBBB) will stand in history as one of the most impactful and disruptive initiatives of the second Trump Presidency. Spanning close to 900 pages, it took shape after months of gruesome negotiations and political maneuvering in Congress. It finally passed by narrow margins in the Senate and House, with 51-50 and 218-214 votes respectively, before President Trump signed it into law on July 4th, the US Independence Day.

At its core, the bill enacts significant changes to the US tax code, extending and expanding tax cuts for high income individuals and corporations, while scaling back funding for safety-net programs, and re-defining spending priorities. The reforms sparked intense debates over its distributional impact and long-term sustainability. Given the magnitude and span of the OBBB, its macroeconomic implications are substantial in scale, and wide-ranging in scope. In this article, we analyse the main aspects of the OBBB along three key dimensions.

First, the bill is set to have a meaningful expansionary impact on the economy over the next decade. According to estimates by the Congressional Budget Office (CBO), real GDP would increase on average by 0.5% over the 2025-2034 period, relative to a scenario without the implementation of the bill. This is a relevant impact on the economy, considering that average annual economic growth in the US has been 2.2% over the last two decades.

The effects would be largest in the short term, with the bill boosting GDP by 0.9% in 2026. The initial push in economic activity would come to a large extent from an increase in aggregate demand, due to higher disposable income for more prosperous households, and items that incentivize investments. Beyond 2026, lower tax rates will improve the incentives to work, increasing labour participation and working hours and, therefore, promoting growth. Overall, the different growth mechanisms point to a positive and significant boost to economic activity.

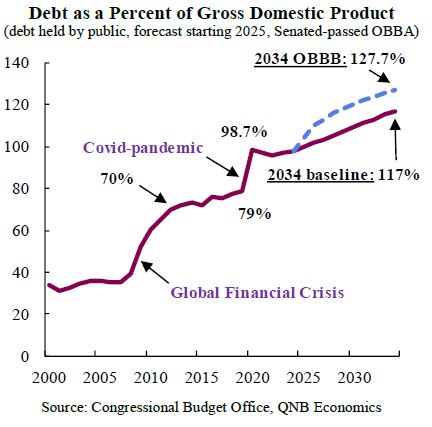

Second, the OBBB will substantially increase the US federal deficit and the path of debt in the coming years. The bill includes a battery of measures that will put pressure on public finances, including the extension of tax cuts, reduced corporate tax revenues, and expanded deductions. On the other hand, some spending cuts are included, mainly targeting entitlements and safety-net programs, but are smaller in relative terms. Over the period between 2025 to 2035, the bill would add an estimated USD 4.6 trillion to the deficits. As a result, federal debt is expected to reach close to 128% of GDP by 2034, its historical maximum. This far surpasses the 119% mark reached in 1946, when the country was absorbing the costs of the World War II economy and the immediate post-war recession.

The sizable increase in the volume of US Treasury debt will certainly test the appetite of international markets, leading to a rise in interest rates. The increase in the supply of Treasury instruments will result in a fall in their price, and therefore an increase in yields. The CBO and Yale Budget Laboratory estimate the OBBB will increase interest rates on 10-year Treasury notes by an average 14 to 30 basis points (b.p.) over the period 2025-2034. This increase in debt costs is not negligible, but it is not exceptionally disorderly considering fluctuations in yields that are typically observed on any given year. Although the upward shift in the trend of debt is substantial and raises some long-term sustainability concerns which eventually need to be addressed, it is unlikely that these dynamics will generate major disruptions in financial markets over the next 10 years.

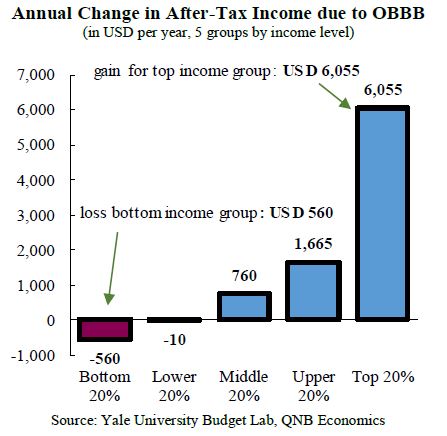

Third, the new legislation entails a significant redistributional impact across households. Through various channels, the net distributional effects of the OBBB are regressive. In other words, it will benefit higher-income households, while reducing support for lower-income households. Specifically, households at the lowest 20% of the income distribution stand to lose USD 560 per year, about 2.3% of their after-tax income. The losses for this group will come mainly as a result of cuts to Medicaid and safety-net programs, such as the Supplemental Nutrition Assistance Program.

Households at the higher segments of the income distribution are less affected by medical and safety-net policies, but are set to gain significantly from the extension of the otherwise expiring income tax provisions of the Tax Cuts and Jobs Act (TCJA). This act includes provisions considering lower tax rates, as well as higher deductions and personal exemptions. For households at the highest 20% of the income distribution, the annual gain on average would reach a sizable USD 6,055 per year, an improvement of 2.4% of after-income tax for this group. For the intermediate segments of the distribution, the household gains from the TCJA extension become larger than the losses from medical and support programs. While middle-income families will see on average modest gains from the tax reforms, the overall structure of the bill shifts fiscal resources towards wealthier households.

The OBBB sets the stage for wide-ranging tax, spending, and structural provisions, with lasting economic implications for the US. All in all, the bill provides a sizable boost to the economy, although at the cost of a rising debt trajectory, while introducing significant distributional shifts.

Download the PDF version of this weekly commentary in

English

or

عربي